Market Overview 2025-2033

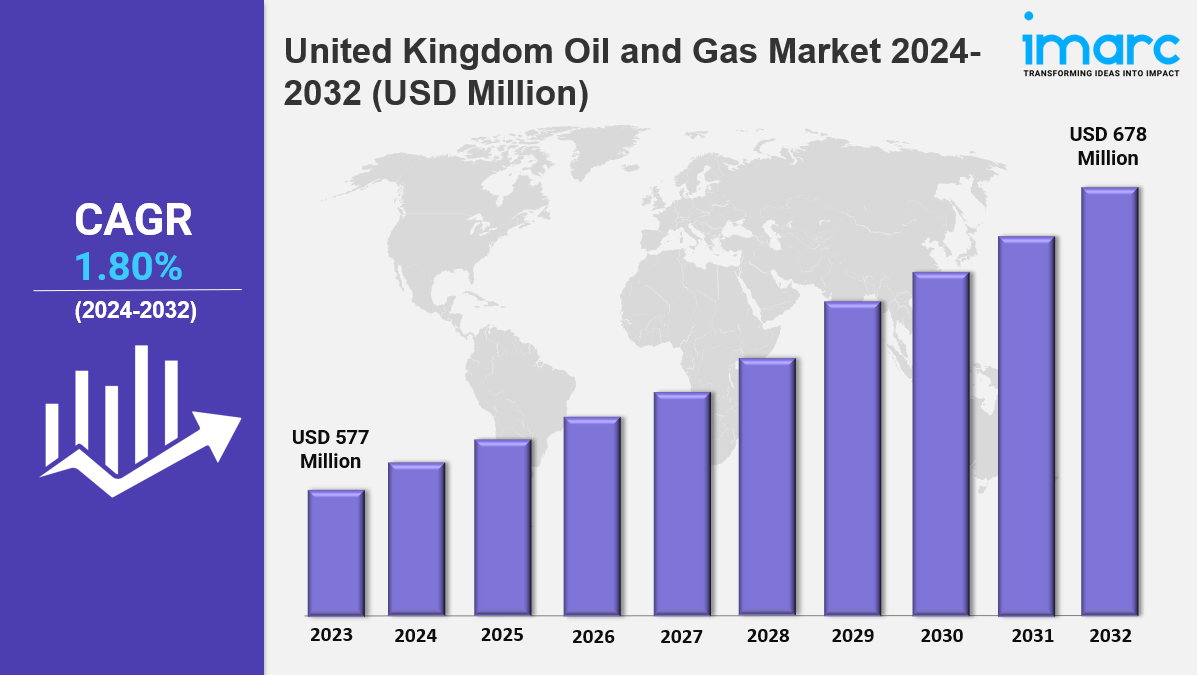

The United Kingdom oil and gas market size reached USD 577 Million in 2023. Looking forward, IMARC Group expects the market to reach USD 678 Million by 2032, exhibiting a growth rate (CAGR) of 1.80% during 2024-2032. The market is evolving due to increasing energy demand, ongoing exploration and production activities, and a shift towards cleaner energy solutions. Government policies, technological advancements, and sustainability initiatives are key factors driving industry growth.

Key Market Highlights:

✔️ Strong market growth driven by increasing energy demand and exploration activities

✔️ Rising investments in offshore drilling, LNG, and renewable energy integration

✔️ Expanding government policies supporting energy transition and sustainability initiatives

Request for a sample copy of the report: https://www.imarcgroup.com/united-kingdom-oil-gas-market/requestsample

United Kingdom Oil and Gas Market Trends and Drivers:

The UK oil and gas market is facing major changes. Global decarbonization efforts are clashing with energy security needs. After the 2022 energy crisis, the UK government reaffirmed its net-zero targets. This led to stricter emissions rules and less funding for fossil fuel projects. By mid-2024, major companies like BP and Shell sped up their divestment from North Sea oilfields. They are now investing in offshore wind, hydrogen, and carbon capture projects. This shift has created two opposing trends. Exploration activities are declining in mature areas like the North Sea. At the same time, hybrid projects are gaining attention.

BP’s “blue hydrogen” project in Teesside, which blends carbon capture and natural gas, is one example. In order to increase short-term productivity, smaller independent businesses are also purchasing old assets. They are profiting from high oil prices brought on by OPEC+ supply constraints. The conflict between short-term financial gain and energy transition objectives reveals a fragmented market. Strategic agility is essential to remaining competitive in this environment. The UK’s energy security has changed as a result of geopolitical tensions, particularly the ongoing conflict between Russia and Ukraine and the instability in the Middle East. Reliance on UK gas exports rose in 2024 as a result of the EU’s progressive embargo on Russian LNG. Compared to the previous year, pipeline flows to Europe increased by 18%.

New infrastructure investments have been spurred by the increase in demand. For instance, the Isle of Grain LNG terminal is growing, and the Rough gas storage facility is reopening. However, important projects like the Rosebank oilfield development have been delayed due to supply chain problems and labor disruptions. Additionally, the UK is working to lessen its dependency on foreign gas. Innovation in the exploitation of domestic shale gas has been fueled by this effort. Nevertheless, there is still popular resistance and regulatory obstacles. A market in transition is indicated by the combination of local operational concerns and geopolitical dangers. Innovation is being fueled by temporary supply shortages, but long-term stability is still up in the air.

Technological advancements are changing the UK’s oil and gas sector. These innovations help operators improve production while meeting environmental standards. By late 2024, AI-driven predictive maintenance systems cut offshore drilling downtime by 30%. Also, blockchain platforms improved supply chain transparency for tracking Scope 3 emissions. The use of modular carbon capture, utilization, and storage (CCUS) systems, like Equinor’s “Northern Lights” project, allows smaller fields to reach net-negative emissions. This supports the UK’s Carbon Budget Delivery Plan.

Furthermore, progress in subsea robotics and drone surveillance has reduced inspection costs by 40%. This extends the life of aging infrastructure. These innovations are more than just upgrades; they are strategic necessities. Companies like Harbour Energy are using digital twins to optimize reservoir management. This approach helps them secure funding from ESG-focused investors. The United Kingdom oil and gas market share must balance energy security, sustainability, and tech changes. A key trend is the rise of “transition fuels.” Natural gas serves as a bridge to renewables. In 2024, gas-fired power generation in the UK reached 42% of the energy mix. This increase came from retiring coal plants and fluctuating renewable output.

This dependence has led to investments in floating LNG terminals and bidirectional pipelines to stabilize supply. At the same time, the North Sea Transition Authority’s carbon storage licensing rounds have attracted £4 billion in private equity. This shows a shift from extraction to reducing emissions. Another defining trend is the convergence of oil and gas with renewable ecosystems. Hybrid projects, such as Repsol’s offshore wind-powered oil rigs in the Shetland Basin, exemplify this integration.

Policy frameworks, like the Energy Security Act of 2024, encourage cross-sector collaboration. They offer tax breaks for companies that convert oil infrastructure for hydrogen or geothermal use. However, workforce challenges are significant. By mid-2025, 35% of skilled labor in the sector will shift to renewables, creating talent gaps in upstream operations. Looking ahead, the market’s path depends on clear regulations and smart capital allocation. The UK plays a key role in Europe’s energy landscape. Its success in managing fossil fuel decline alongside green industrialization will shape its competitiveness in a net-zero future.

United Kingdom Oil and Gas Market Segmentation:

The report segments the market based on product type, distribution channel, and region:

Study Period:

Base Year: 2023

Historical Year: 2018-2023

Forecast Year: 2024-2032

Breakup by Type:

- Upstream

- Midstream

- Downstream

Breakup by Application:

- Offshore

- Onshore

Breakup by Region:

- London

- South East

- North West

- East of England

- South West

- Scotland

- West Midlands

- Yorkshire and The Humber

- East Midlands

- Others

Competitive Landscape:

The market research report offers an in-depth analysis of the competitive landscape, covering market structure, key player positioning, top winning strategies, a competitive dashboard, and a company evaluation quadrant. Additionally, detailed profiles of all major companies are included.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

{kind=link}