Market Overview 2025-2033

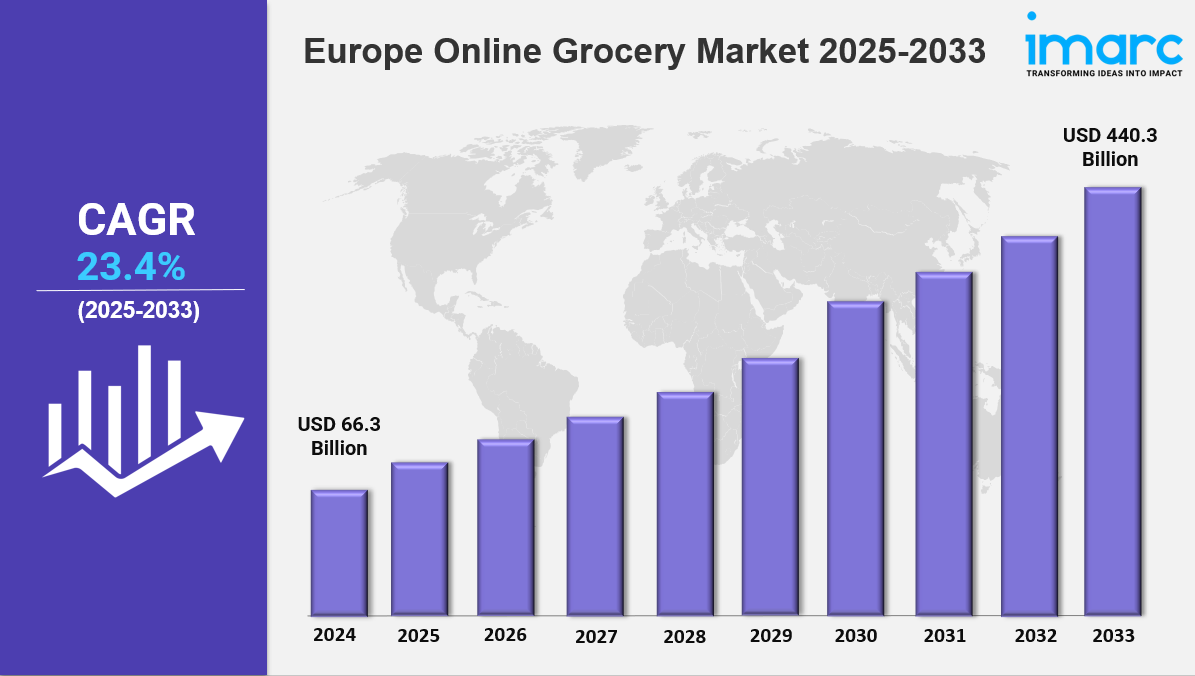

The Europe online grocery market size was valued at USD 66.3 Billion in 2024. Looking forward, IMARC Group estimates the market to reach USD 440.3 Billion by 2033, exhibiting a CAGR of 23.4% from 2025-2033. The market is expanding rapidly due to growing e-commerce adoption, changing consumer preferences, and convenience-driven shopping habits. Technological advancements, quick delivery services, and digital payment solutions are key factors driving industry growth.

Key Market Highlights:

✔️ Strong market growth driven by increasing digital adoption and demand for convenience

✔️ Rising preference for fresh, organic, and subscription-based grocery deliveries

✔️ Expanding investments in AI-driven logistics, dark stores, and quick commerce solutions

Request for a sample copy of the report: https://www.imarcgroup.com/europe-online-grocery-market/requestsample

Europe Online Grocery Market Trends and Drivers:

The Europe online grocery market is growing rapidly and transforming how people shop for food. More retailers are turning to smart technology to make shopping easier, faster, and more personal. Companies like Picnic in the Netherlands and Rohlik in Central Europe are using advanced tools to learn what their customers love. These tools can spot habits—like a family in Milan restocking olive oil every two weeks or a summer spike in berry sales in Stockholm. Some platforms even suggest recipes and help plan meals based on past orders.

In the UK’s online grocery scene, Ocado launched its Smart Basket tool in 2024. It remembers what shoppers usually buy and even checks the weather to make timely suggestions—like reminding customers in Amsterdam to grab hot chocolate on a chilly day. Since launching, it’s helped reduce abandoned carts by 27%. These types of innovations are a big reason why the Europe online grocery market size continues to climb. In fact, a recent report revealed that over €2.3 billion has been invested in personalization tools by leading grocery chains.

Sustainability is also a top priority. With new EU regulations aimed at cutting delivery emissions, companies are finding creative solutions. Carrefour, for example, opened small local warehouses in Paris, and now 68% of their orders are delivered within 90 minutes using electric bikes—cutting pollution by 62% in just one year. Across the Nordics, Coop Norway and Mathem Sweden are teaming up to save energy by sharing cold storage facilities. In the UK, Waitrose customers are choosing “Green Slot” deliveries, where they wait a bit longer for more eco-friendly time slots.

But going green comes at a cost. In early 2024, delivery fees rose by 8.4%, and many stores have introduced small “eco-premiums” for faster or low-emission deliveries. Another major shift in the European online grocery market is the growing number of senior shoppers going digital. In Italy, where 32% of the population is over 60, retailers are creating new services tailored to older customers. Esselunga has trained more than 210,000 seniors to shop online, while Portugal’s Continente offers voice-assisted shopping in regional dialects and simplified meal kits designed for ease of use.

Spain’s Compra Dorada program gives seniors €15 monthly to help with online grocery costs, which has driven a surge in adoption—online usage among those over 70 jumped from 19% to 34% in just six months. Today, older shoppers account for 38% of the growth in online grocery sales in Southern Europe. Still, digital access isn’t equal everywhere—only 61% of rural Greek villages have reliable internet, which remains a challenge for expanding the European online grocery market share.

Looking ahead, 2024 is a pivotal year. Experts predict that online grocery sales will make up more than 20% of all food shopping in the EU. This shift is powered by several key trends: habits formed during the pandemic, the rise of “dark stores” designed for quick delivery, and large-scale cross-border mergers. For example, Ahold Delhaize acquired Ulabox in Spain, and Migros bought Barbora in Lithuania—moves that are helping brands expand and operate more efficiently.

Even though the Europe online grocery market size is set to hit €148 billion in 2024—an 18% increase from last year—profit margins remain tight at around 3.2%, due to the high costs of delivery. To stay competitive, grocers are focusing on cost-saving strategies like automation, AI-powered logistics, and expanding store-brand offerings. By 2025, store-brand items could make up 35% of all online grocery products. With strong demand, smarter tools, and sustainability at the forefront, the Europe online grocery market share is poised for long-term growth. It’s clear that online grocery shopping isn’t just a convenience anymore—it’s becoming the new normal across the continent.

Europe Online Grocery Market Segmentation:

The market report offers a comprehensive analysis of the segments, highlighting those with the largest Europe online grocery market growth. It includes forecasts for the period 2024-2032 and historical data from 2018-2023 for the following segments.

Study Period:

Base Year: 2024

Historical Year: 2019-2024

Forecast Year: 2025-2033

Analysis by Product Type:

- Vegetables and Fruits

- Dairy Products

- Staples and Cooking Essentials

- Snacks

- Meat and Seafood

- Others

Analysis by Business Model:

- Pure Marketplace

- Hybrid Marketplace

- Others

Analysis by Platform:

- Web-Based

- App-Based

Analysis by Purchase Type:

- One-Time

- Subscription

Country Analysis:

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

Competitive Landscape:

The market research report offers an in-depth analysis of the competitive landscape, covering market structure, key player positioning, top winning strategies, a competitive dashboard, and a company evaluation quadrant. Additionally, detailed profiles of all major companies are included.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: [email protected]

Tel No:(D) +91 120 433 0800

United States: +1-631-791-1145

{kind=link}